FHA Loans: Understanding Requirements For Bad Credit Home Buyers

FHA Loans: Property Standards, Appraisals, and Repair Considerations

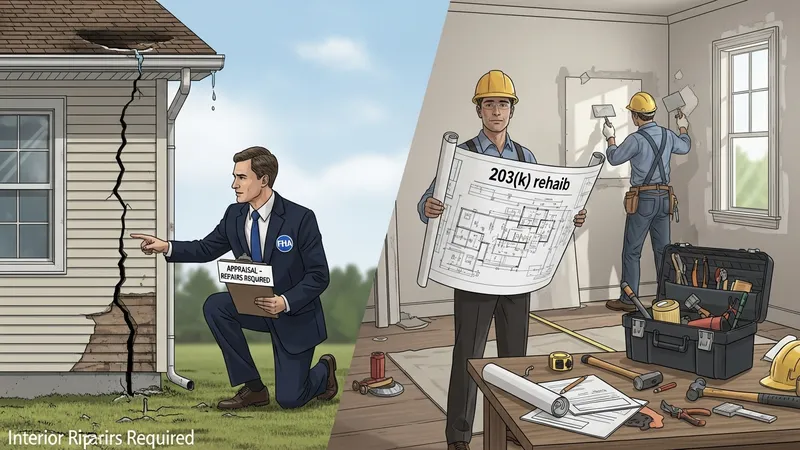

FHA loans generally require properties to meet minimum property standards intended to ensure safety, security, and soundness. Appraisers following FHA protocols evaluate structural systems, water intrusion, heating and cooling, and other health and safety items. If a property requires repairs for FHA compliance, the loan may be delayed until required corrections are made or an alternative financing path that includes renovation costs may be used.

The FHA 203(k) rehabilitation option permits certain repair and renovation costs to be included in the mortgage amount, which can be useful when a property’s condition would otherwise disqualify it. This path requires detailed plans, contractor estimates, and a specialized appraisal that accounts for the estimated post-repair value. Timing for disbursing renovation funds and completing work is typically governed by program rules and lender procedures.

Appraisal findings that identify health or safety defects often result in repair requirements that must be satisfied before final endorsement. Some repairs can be completed post-closing under escrowed conditions when permitted by the program and lender, while other deficiencies must be corrected on-site before funding. Understanding the scope of required corrections upfront may help borrowers and sellers plan timelines and budgets for closing.

For homes in need of significant work, alternative arrangements such as renovation mortgages, seller concessions for repairs, or contingent repair escrows may be considered in the underwriting process. Each option has documentation and inspection requirements; therefore, coordinating among real estate agents, contractors, appraisers, and lenders is often essential to align expectations and meet program standards without unnecessary delay.