Hotel Jobs In Switzerland: Understanding Work Permits, Visas, And Legal Framework

Employment contracts, regulation, and social insurance in the hotel sector

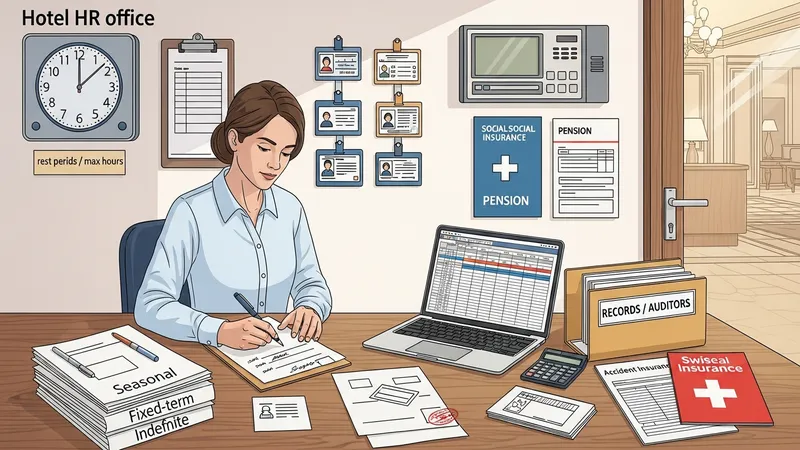

Employment contracts in the hospitality sector usually specify working time, remuneration, probation periods, and termination conditions. Swiss labour law sets baseline protections such as limitations on excessively long working hours and provisions for rest periods, but sector-specific terms may be determined by collective labour agreements or employer policies. Contracts often note whether employment is seasonal, fixed-term, or indefinite, and such distinctions commonly affect social-insurance registration and entitlement accruals like paid leave and pension contributions.

Employers are typically obliged to register employees for national social insurance schemes that cover old-age and survivors’ insurance, disability insurance, and unemployment contributions. Occupational pension plans and accident insurance are commonly part of statutory coverage. Payroll deductions and employer contributions to these schemes are standard components of cost and compliance. Employers commonly maintain payroll and employment records to document compliance with statutory and contractual obligations for employment authorities and auditors.

Collective labour agreements may apply in parts of the hospitality sector and can set standardised minimum wages, overtime compensation rates, and sector-specific working-time arrangements. Where such agreements exist, they usually influence contract terms and dispute resolution mechanisms. Employment law also typically provides frameworks for notice periods, severance in certain circumstances, and mechanisms for resolving disagreements through labour courts or mediators, depending on the nature of the dispute and the parties involved.

Taxation on salaries is generally handled through payroll withholding and canton-specific tax rules for residents and cross-border workers. The tax treatment of allowances such as accommodation or meals can differ by canton and individual circumstances. Employers and employees commonly consult cantonal tax offices or neutral guidance to confirm withholding obligations and tax residency criteria, as tax status may affect net income and social-security entitlements over time.